It has been a good year for the Big Bulls in the market, despite the bitter experience for small caps.

China, Brexit, Trump trigger wild ride for global equities

Rich get richer as fortunes whipsaw through $4.8 trillion

In a year when populist votersreshapedpower and politics across Europe and the U.S., the world’s wealthiest people are ending 2016 with $237 billion more than they had at the start.

Triggered by disappointing economic data from China at the beginning, the U.K.’s vote to leave the European Union in the middle and the election of billionaire Donald Trump at the end, the biggest fortunes on the planet whipsawed through $4.8 trillion of daily net worth gains and losses during the year, rising 5.7 percent to $4.4 trillion by the close of trading Dec. 27, according to the Bloomberg Billionaires Index.

“In general, clients rode through the volatility,” said Simon Smiles, chief investment officer for ultra-high-net-worth clients at UBS Wealth Management. “2016 ended up being a spectacular year for risk assets. Pretty remarkable given the start of the year.”

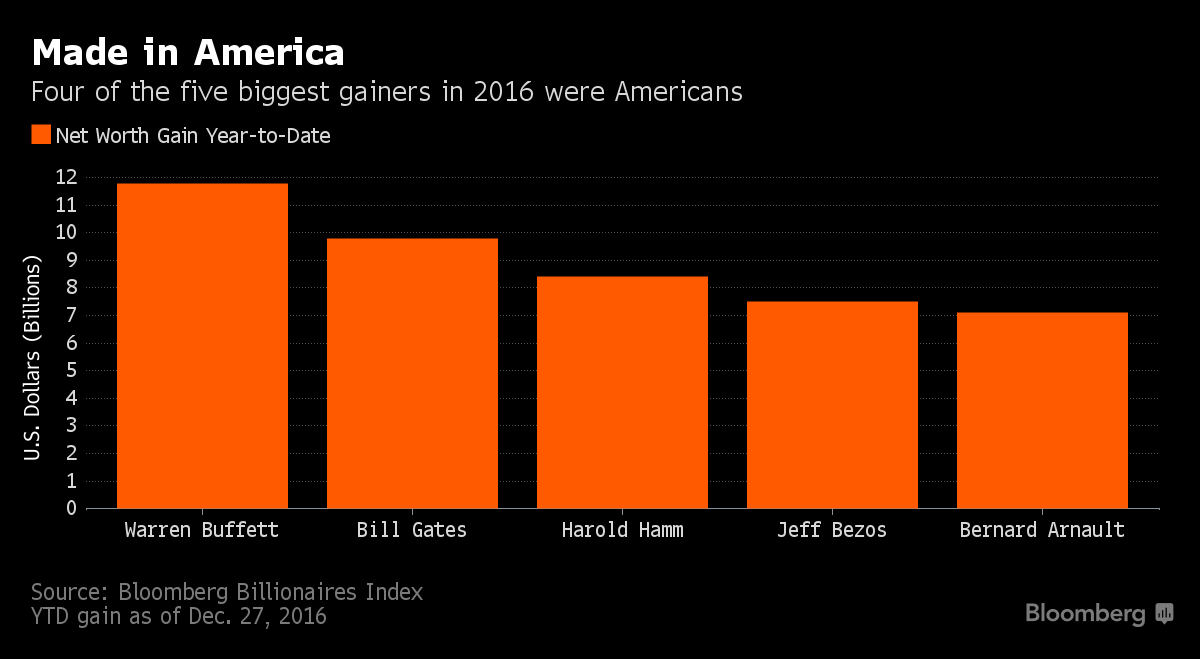

The gains were led by Warren Buffett, who added $11.8 billion during the year as his investment firm Berkshire Hathaway Inc. saw its airline and banking holdings soar after Trump’s surprise victory on Nov. 8. Buffett, who’s pledged to give away most of his fortune to charity, donated Berkshire Hathaway stock valued at $2.6 billion in July.

Berkshire Bonanza

Warren Buffett

Photographer: Daniel Acker/Bloomberg

The U.S. investor reclaimed his spot as the world’s second-richest person two days after Trump’s victory ignited a year-end rally that pushed Buffett’s wealth up 19 percent for the year to $74.1 billion.

“2016’s been event-driven with global news driving prices rather than fundamentals,” said Michael Cole, president of Ascent Private Capital Management, which has about $10 billion of assets under administration. “The belief that Trump is going to come in and deregulate big parts of the economy is driving the markets right now.”

The individual gains for the year were dominated by Americans, who had four of the five biggest increases on the index, including Microsoft Corp. co-founder Bill Gates, the world’s richest person with $91.5 billion, and oilman Harold Hamm.

The country’s richest were largely opposed to a Trump presidency during the election, including Dallas Mavericks owner Mark Cuban, who told the media in May that stocks could fall as much as 20 percent if Trump were to win the election.

Wealth Administration

U.S. billionaires -- including Buffett -- favored Trump’s rival Hillary Clinton. Still, they profited from his victory when they added $77 billion to their fortunes in the post-election rally fueled by expectations that regulations would ease and American industry would benefit.

The New York real estate mogul is building a cabinet heavy on wealth and corporate connections, and light on government experience, a mix that hedge fund billionaire Ray Dalio said last week would unleash the "animal spirits" of capitalism and drive markets even higher. Dalio is the world’s 63rd-richest person with $14.1 billion.

Wilbur Ross

Photographer: Drew Angerer/Getty Images

Investors and executives welcomed Trump’s picks, including billionaire Wilbur Ross to lead the Department of Commerce and former Goldman Sachs Group Inc. executive Steven Mnuchin as his Treasury secretary, who have a combined net worth of at least $5.6 billion, according to the index.

“You know, I was not opposing Trump as much as most people,” Saudi Arabian billionaire Mohamed Bin Issa Al Jaber said in a Dec. 11 interview. “He’s capable and -- as a businessman -- he’s shrewd about the bottom line. The people he’s surrounding himself with have baggage but they’re also successful and shrewd.”

France’s Bernard Arnault was the sole non-American representative among the five best performers, adding $7.1 billion to take his fortune to $38.9 billion. His LVMH Moet Hennessy Louis Vuitton SE said the Chinese luxury-goods market is improving.

Gates remained the world’s richest person throughout the year. Amancio Ortega, Europe’s richest person and founder of the Zara clothing chain, was in second place on the index for most of the year until he ceded it to Buffett in November. Ortega, who dropped $1.7 billion in 2016, is the world’s third-richest person with $71.2 billion.

Harold Hamm

Photographer: Andrew Harrer/Bloomberg

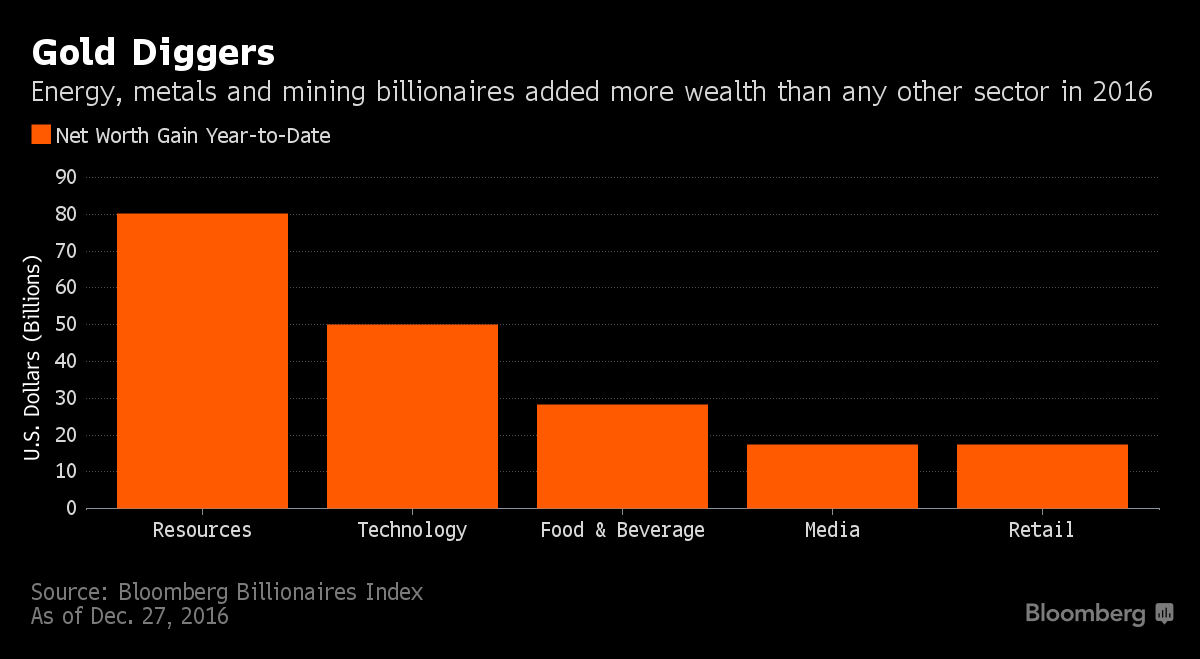

Wildcatter Hamm’s fortune was propelled by a strengthening oil price and expectations a Trump administration will slash fossil-fuel regulations. Hamm added $8.4 billion to more than double his fortune to $15.3 billion. He led the 49 energy, metals and mining billionaires, who were the best-performing category on the ranking, adding $80 billion and reversing the $32 billion fall they had in 2015.

Billionaire brothers Charles and David Koch each dropped $2 billion after Koch Industries reported on its website that annual revenue is estimated to be "as high as $100 billion," compared with the estimate of "as much as $115 billion" that the conglomerate published on the site previously. Company spokesman Rob Carlton stated in a Nov. 17 e-mail that Koch revenue fluctuates with the price of commodities.

Technology fortunes were the second-best performing on the ranking, with 55 billionaires adding $50 billion to their fortunes over the year, despite worries that a Trump presidency might introduce policies that could hurt their companies.

“I think we’ll have to see what the policies of the administration are,” Google co-founder Sergey Brin told the media gathered on the red carpet of the annual Breakthrough Prize gala in Silicon Valley in December. “I certainly hope they will be pro-science, pro-technology and all the things this world has really benefited from.”

Jeff Bezos

Photographer: Patrick Fallon/Bloomberg

Amazon.com Inc. founder Jeff Bezos, who doubled his fortune to $60 billion in 2015, led gains among technology executives again this year, rising $7.5 billion in 2016 on robust sales growth at the online retailer. He was followed by Facebook Inc. co-founder Mark Zuckerberg, who added $5.4 billion.

Hidden Wealth

Some of the industry’s biggest relative gains went to the founders of the world’s leading startups, such as Uber Technologies Inc.’s Travis Kalanick and Snap Inc.’s Evan Spiegel. The so-called "unicorn" billionaires, which include Spotify Inc. co-founder Martin Lorentzon, who was identified as a billionaire for the first time in 2016, secured a series of mammoth funding rounds while moving closer to testing their fortunes on the public markets.

Other billionaires uncovered by the Bloomberg index in 2016 included the father and son behind Jose Cuervo tequila, New York real estate developer Axel Stawski and Kosovo construction tycoon Behgjet Pacolli.

Marcos Galperin

Photographer: David Paul Morris/Bloomberg

The index also unveiled 11 surviving family members of reclusive Thai entrepreneur Chaleo Yoovidhya, the inventor of Red Bull, whose heirs share a combined $22 billion net worth, the world’s largest energy-drink fortune. Three billionaires emerged in Argentina, including the country’s first technology billionaire Marcos Galperin, as markets rose on enthusiasm for President Mauricio Macri’s finance-friendly economic policies.

Wang Jianlin

Photographer: Justin Chin/Bloomberg

Most fortunes outside of the U.S. didn’t get the same boost from Trump’s victory, and were hurt by fluctuating commodities prices and the rise of the dollar, the currency used for the Bloomberg ranking. Nine of the 10 biggest decliners in 2016 were from outside the U.S., led by China’s second-richest person, Wang Jianlin, who lost $5.8 billion. Wang ended the year as the world’s 21st-richest person with $30.6 billion.

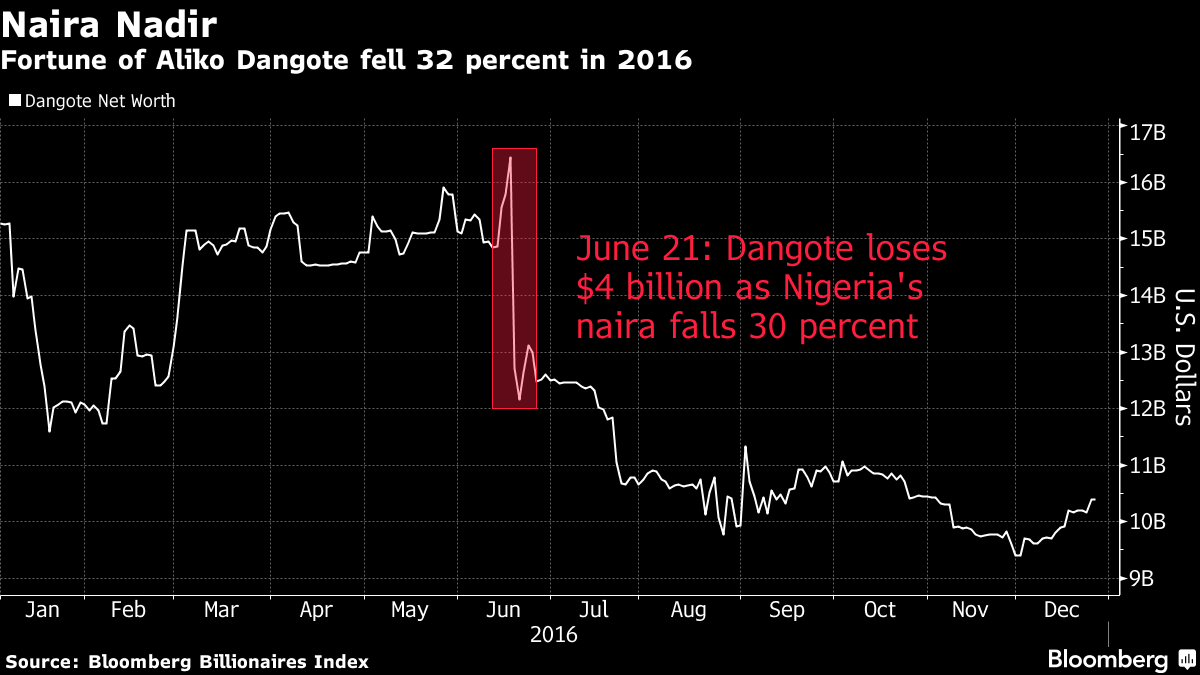

Nigeria’s Aliko Dangote, the richest person in Africa, lost $4.9 billion or one-third of his wealth as the combined effect of falling oil prices and the June devaluation of the naira pushed him to No. 112 with $10.4 billion. Dangote was the world’s 46th-richest person in June.

Saudi Arabia’s Prince Alwaleed Bin Talal Al Saud fell $4.9 billion, a 20 percent drop. Alwaleed said in November that all of his stakes in public companies including Citigroup Inc. are potentially for sale, reversing a longstanding policy that some of his most prized shareholdings were “forever.”

Chinese Downturn

Wealth creation in China turned negative for the first time since the inception of the Bloomberg index five years ago, with the country’s richest losing $11 billion in 2016 amid a slump in the Shanghai Shenzhen CSI 300 index and a 7 percent decline for the yuan against the dollar.

Alibaba Group Holding Ltd. founder Jack Ma closed the year with $33.3 billion, adding $3.6 billion in 2016. He dropped in and out of his place as Asia’s richest person for the first four months of the year before claiming it for good in May after Alibaba’s finance affiliate, which is laying the groundwork for an initial public offering expected as soon as next year, completed a record $4.5 billion equity fundraising round.

China has 31 billionaires on the index with $262 billion, trailing the U.S.. which has 179 billionaires who control $1.9 trillion, and Germany, whose 39 individuals have $281 billion. Russian billionaires also began to put the negative effects of U.S. and European sanctions behind them, reversing the combined $63 billion declines for 2014 and 2015 and adding $49 billion in 2016.

Looking Ahead

Wealth managers for the world’s richest are girding themselves for similarly frenetic start to 2017 as the seismic changes voters demanded this year start to take shape.

"Expect the unexpected," said Sabine Kaiser, founder of SKadvisory, which advises family offices on venture capital and private equity. "I don’t think family offices are overly concerned or getting too nervous but after Brexit and Trump they’ve resigned themselves to market volatility."

More than 500,000 jobs lost in two years as factories close

Improving power, gas supply may halt export drop: central bank

A neglected waiting area, empty reception and dim lights greet visitors at what used to be the biggest textile factory in the northern industrial area of Pakistan’s economic hub.

At its peak Al-Abid Silk Mills Ltd. employed 7,600 employees in Karachi, now only a handful can be seen in the near-abandoned garment workshop. It’s one of hundreds that have shut down over the past few years, contributing to Pakistan’s exports falling to their lowest in six years.

An abandoned textile factory.

Photographer: Asim Hafeez/Bloomberg

Exporters from South Asia’s second-largest economy, including textile manufacturers who account for more than half of all overseas shipments, say buyers have shifted to countries including Bangladesh and Vietnam as continual power outages impede their ability to meet order deadlines, while complaining that the government has provided scant support.

“The government has never planned how we need to go forward with the textile industry,” Naseem Sattar, the 80-year-old chief executive officer of Al-Abid, said as he smoked in his office in the derelict plant. “Such a factory is considered a national asset and we got no help.”

Despite a pick up in economic growth after the government submitted to an International Monetary Fund program in 2013 to avert a balance of payment crisis, Pakistan’s exports have fallen as global demand slows and the nation tries to overcome an energy shortage. Overseas shipments for the year through June fell to $21 billion, the lowest level since 2010, according to Pakistan Bureau of Statistics.

“Internally you have constraints on energy and then manufacturing keeping exports down,” said Turab Hussain, head of the economics department at the Lahore University of Management Sciences. “If oil prices go up and exports don’t pick up there will be pressure on your balance of payments and currency.”

About 100 member factories have shut down and at least 500,000 people have lost jobs in the past two years, according to Saleem Saleh, acting secretary general of All Pakistan Textile Mills Association, the biggest contributor to the nation’s textile exports. About two-thirds of the members of the Pakistan Bedwear Exporters Association have stopped working in the past five years, according to its head Shabir Ahmed.

Most factories shutting down are small or mid-sized plants unable to bear the extra cost of prolonged power outages. Meanwhile, larger factories have invested in their own power, including diesel generators, to cope with the nation’s electricity deficit of about 3,000 megawatts.

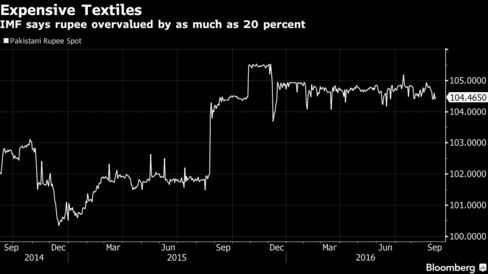

The IMF, which is set to conclude its three-year, $6.6 billion loan program with Pakistan at the end of this month, is pointing to a number of causes, including the local currency it says is overvalued by as much as 20 percent.

“The continued decline in exports is a cause for concern, to a good extent that’s due to a fall in international prices for cotton and other commodities,” Harald Finger, the IMF’s mission chief for Pakistan, said in a July interview. Domestically “there are security issues, there are continued power outages, even though they are declining now, that’s still a factor. There are issues around the business climate, and so on, and also one of these factors is also the real effective exchange rate.”

Yarn bobbins sit in a closed textile mill.

Photographer: Asim Hafeez/Bloomberg

About half of the Pakistan’s exports are shipped to six countries, while 40 percent of total textile exports are primary commodities, including cotton yarn sent to China, Minister of Commerce Khurram Dastgir Khan told lawmakers in Islamabad’s parliament on Sept. 5. Pakistan’s apparel exports grew less than half the pace of Bangladesh and Vietnam before the recent fall during 2005 to 2012, according to World Bank data.

For buyers, Pakistan’s competitors are also more alluring due to the country’s tarnished security image after years of insurgency, bombings and violence.

Security Perception

“If you can get the same price in Vietnam or India or Bangladesh, I think it’s still the case that most purchasers will still choose the other countries because their purchasing managers dare to go there,” said Mattias Martinsson, the Stockholm-based chief investment officer at Tundra Founder AB, which holds about $160 million in Pakistani stocks. “They can go freely around and don’t have to be afraid” which isn’t their perception of Pakistan, he said.

Even so, the country’s security situation has improved with an army push against insurgents after more than 100 students were killed by the Pakistani Taliban at a military school in 2014 in the northern city of Peshawar. About 449 people died in terrorist-related violence last year, the lowest in 10 years, according to the South Asia Terrorism Portal.

The government recognizes the industry’s malaise and Prime Minister Nawaz Sharif on a visit to Karachi on Sept. 8 said boosting exports is a top priority and his administration will soon announce relief measures.

‘Cannot Ignore’

Sharif is also pegging his 2018 re-election prospects on ending the daily power blackouts, relying on a surge of Chinese investment and projects worth $46 billion that were announced last year.

“Economic growth and exports are interlinked,” Sharif said. “We cannot afford to ignore our exports.”

A worker operates a sewing machine at a textile manufacturer in Karachi.

Photographer: Asim Hafeez/Bloomberg

Pakistan already announced in June azero-rated sales tax regime for five export industries, including textiles. Borrowing has become more attractive with the discount rate at its lowest in more than four decades. Sharif this month asked the ministry of commerce to arrange a duty-free import of five million bales of cotton to plug a domestic shortage this year.

Despite these measures, State Bank of Pakistan Governor Ashraf Mahmood Wathra says the nation needs to diversify products and exports markets away from those on a declining trend. However, he expects improved electricity and gas supplies this year to stem some of the drop in exports.

‘Very Happy’

“When I speak to industrialists, I see them more comfortable than two-to-three years ago,” Wathra said. Textile exporters complain about tax refunds being delayed by the authorities, but otherwise “they are very happy with the interest rate and refinance rate,” he said.

Sattar, whose factory used to make $100 million annual revenue at its peak, doesn’t agree. He wants to get his plant running again, but is unable to repay loans taken to purchase the milling machines. Sattar is now being hounded by banks and the country’s anti-graft agency, he said.

“If you are drowning, they push you further down,” he said. “Textiles are going away from Pakistan.”

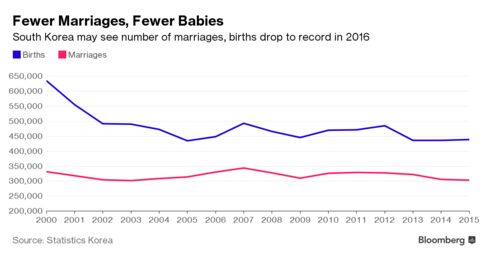

South Koreans are likely to have fewer weddings and babies this year than ever before, part of a demographic shift that risks hobbling the nation’s economy.

The number of marriages and births recorded during the first five months of 2016 hit the lowest levels for the same period in any year since the nation’s statistics office started compiling monthly data in 2000.

The figures underscore the challenge facing the government, which over the past decade has poured 80 trillion won ($72 billion) into efforts to reverse the falling birthrate. Prime Minister Hwang Kyo Ahn said this month that the country faces a crisis that threatens to limit long-term economic growth.

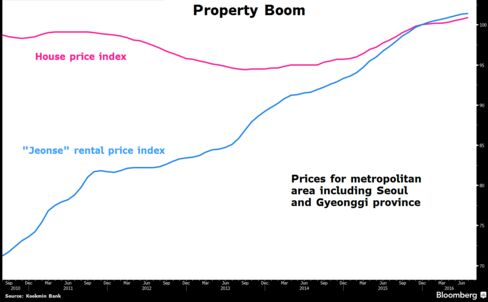

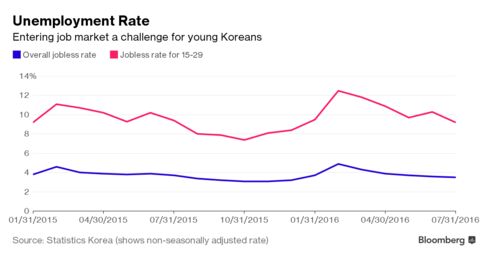

Many young South Koreans say they can’t afford to get married or have children. They cite housing costs as one of the biggest obstacles. Record-low interest rates meant to spur economic growth have fueled a property boom that has priced many of them out of the market. Meanwhile, the unemployment rate among those 15 to 29 years old is 9.2 percent—more than double the national average.

“Previous policies were focused on getting married women to have more babies, but a more fundamental problem could be that young people without jobs are finding it difficult to get married,” said Yoo Jin Sung, a Seoul-based research fellow at the Korea Economic Research Institute. “Youth unemployment is raising the age at which people get married and have their first babies, which can affect the total number of babies they plan to have.”

Women also say South Korea’s corporate culture makes life challenging for working mothers, leaving many reluctant to get married and have children.

Reversing the demographic tide is becoming more urgent. The country will pass two unwelcome milestones next year: its workforce will begin shrinking and people aged 65 and older will outnumber those 14 and below. Without successful government action, the economy’s potential growth rate will fall to 2 percent between 2026 and 2030, from about 2.7 percent now, the Hyundai Research Institute estimates.

The demographic decline is already entrenched: The number of women in their 20s and 30s is expected to fall to about 5.5 million by 2030, down from 7.3 million in 2010, according to the government’s statistics office.